Diversification is key

The first step in our investment management process is selecting a set of asset classes that can be used as building blocks of our client portfolios. When doing this, we look for asset classes that:

- 1 Provide diversification benefits

- 2 Have at least 10-years of investment track record

- 3 Are covered by at least one low-cost, high-quality ETF

The following table shows the asset classes we use in our portfolio and the benefits that each provide.

We do not include commodities or natural resources in our asset class set. The reason is that the Canadian economy, and the Canadian stock market are highly correlated with commodity prices. As such, commodities as an asset class do not offer the same diversification benefits to a Canadian investor as a US or European investor.

Asset Class | Benefits | |

|---|---|---|

| 1 | Canadian Stocks | Growth, long-term inflation protection, diversification |

| 2 | US Stocks | Growth, long-term inflation protection, diversification |

| 3 | International Stocks | Growth, long-term inflation protection, diversification |

| 4 | Emerging Stock Markets | Growth, long-term inflation protection, diversification |

| 5 | Canadian Bonds | Income, diversification |

| 6 | Emerging Market Bonds | Income, diversification |

| 7 | REITs | Inflation Protection, diversification, income |

The optimal asset

allocation for each client

The proportions of each asset class in a client portfolio is a function of the risk-level for that portfolio. In order to determine the appropriate asset class proportions for each risk level, we follow a variation of a methodology developed by Nobel Prize winning economist Harry Markowitz called Mean-Variance Optimization (MVO).

MVO is a mathematical framework that is used by many institutional and sophisticated investors. By using MVO, we can find the optimal combination of assets that maximize returns for each level of risk. The inputs to MVO are expected returns for each asset class, standard deviation of returns, and correlation of returns of asset classes with each other.

The standard deviation and correlation of asset class returns are calculated from the monthly return data for the last 10 years.

We have built internal models to calculate expected returns for each of the asset classes we include in our portfolios. For stocks, our models look at current dividend yields, growth in earnings per share, and long-term price to earnings ratios. For bonds, we look at factors such as current yields and interest rates; long-term interest rate forecasts, and the bond portfolio’s duration and convexity. For REITs, our models look at dividend yields, growth in dividends per share, and the yield spread between real return bonds and REITs.

After calculating the expected returns for each asset class we adjust them for taxes and fees. Our optimization has been run for both taxable and tax-sheltered accounts such as RRSPs and TFSAs. We have found that the tax status of the account makes a small difference in the recommended asset allocation. (The tax status of the account has a more important impact on the recommended funds for the account due to issues relating to withholding taxes.)

In order to account for the uncertainty in the expected returns of our asset classes, and to reduce the optimization’s sensitivity to input parameters, we simulate thousands of possible return scenarios within the constraints of asset class expected returns, standard deviation, and correlations.

For each scenario, we calculate the optimal portfolio. We then use an averaging technique to combine the results of each simulation to arrive at our recommended asset allocation. This process is often called Resampled Mean Variance Optimization in the financial industry.

The model portfolios that we arrive at using this method are less sensitive to changes in input assumptions, and are expected to perform well under different market environments.

Putting it all together

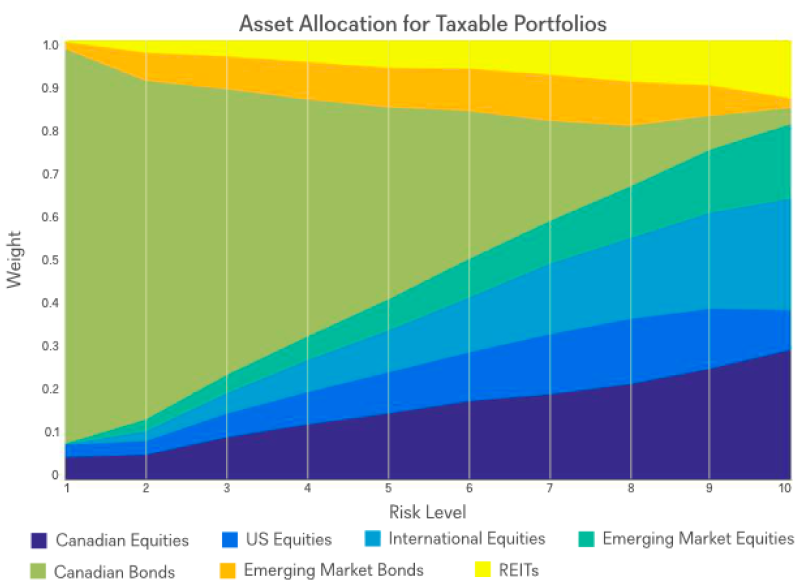

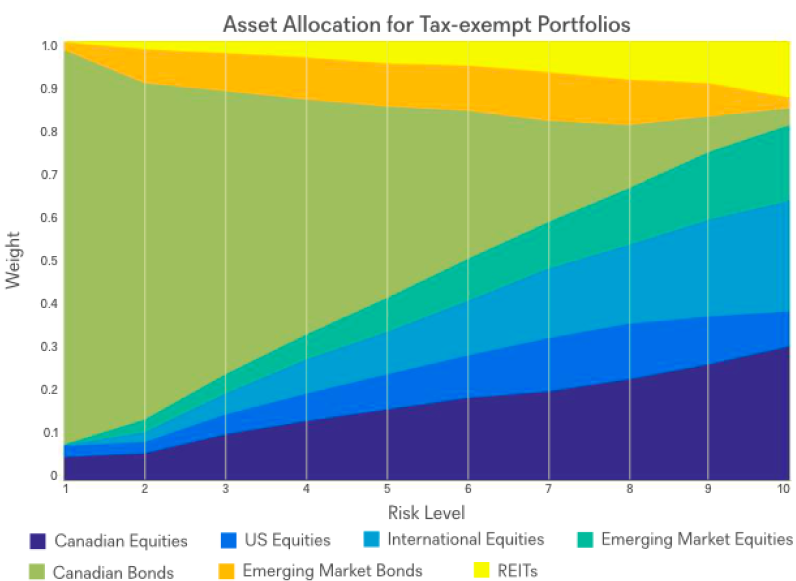

The following charts show the recommended asset allocation for taxable and tax-sheltered accounts at each risk level.

Rebalancing

Having an optimized asset allocation is great, but how do we keep it that way? By rebalancing our clients’ portfolios. Many DIY and professional investors rebalance their portfolios on a time-based schedule. For example, once per year or quarter, those investors review their portfolio’s holdings and rebalance those holdings back to their target asset allocation (or target weights) by selling those assets that are above their target weights and buying more of those assets that are below their target weights.

Rather than only reviewing our clients’ portfolios once per quarter or year, ModernAdvisor’s platform automatically reviews all client accounts on a daily basis. Any accounts that have one or more asset classes, or a cash balance, that is more than 5% above or below their target weight, is rebalanced. For example, if the target weight for Canadian bonds in a portfolio is 30%, and the current weight of Canadian bonds in the account is 24%, the account would need to be rebalanced by selling some of the other asset classes in the account to buy more Canadian bonds. Conversely, if the current weight of Canadian bonds in the account was 36%, the account would need to be rebalanced by selling some of the Canadian bond holding, and buying some of the other asset classes in the account.

What could potentially trigger a rebalancing:

- 1 When the market moves, not all funds go up or down in the same direction or by the same amount. This will result in the weight of some funds exceeding their target, while others could have a weight below their target. If any of the funds have a weight that is more than 5% below or above their target, then the account would be rebalanced by selling the overweight positions and buying the laggards.

- 2 If a client makes a deposit to their account that increases the cash balance to more than a specified threshold, then the account would be rebalanced by buying more of the asset classes that are below their target weights.

- 3 If a client changes their investment goal, timeframe, and/or has a change in their financial situation and updates their profile accordingly, they may be recommended a different risk level than their account is currently invested in. As a result their account would need to be rebalanced.